Mega AI IPOs arriving

Mega AI IPOs arriving

Introduction

As of May 2026, the mega AI IPO story is moving from hype to market reality: Cerebras has already listed with a $5.55 billion IPO and roughly $56 billion valuation, OpenAI and Anthropic are being discussed at near-trillion-dollar valuation levels, Databricks looks like the most financially mature enterprise AI IPO candidate, and CoreWeave remains the key public-market benchmark for AI infrastructure risk. The central issue is not whether investors want AI exposure, because they clearly do, but whether these companies can prove durable revenue, strong margins, manageable compute costs, customer retention, and real productivity gains. “Tokenmaxxing” captures the 2026 corporate obsession with maximizing AI usage, but token consumption alone is not value creation. The real test for AI IPOs will be converting massive AI usage into defensible cash flow rather than just higher cloud bills and inflated valuations.

Let’s dive deep into it.

1. The 2026 AI IPO wave is real, but uneven

By late May 2026, the AI IPO market has moved from rumour to action. Cerebras has already listed, OpenAI is reportedly preparing a confidential IPO filing, Anthropic has raised a massive pre-IPO round, and Databricks is financially IPO-ready but has not yet filed. The key point is that “AI IPO” now covers three different kinds of businesses: model labs, AI infrastructure providers, and AI-enabled enterprise software companies.

2. OpenAI is the symbolic centre of the wave

OpenAI is reportedly laying groundwork for an IPO that could value it at up to $1 trillion. Reuters reported that OpenAI had considered raising at least $60 billion at the low end in preliminary IPO discussions, with timing possibly in the second half of 2026, though plans may change. A later Reuters report on 20 May 2026 said OpenAI was preparing to confidentially file soon and was last valued at $852 billion.

3. OpenAI’s IPO size could reset global IPO history

If OpenAI raises $60 billion or more, it would not be a normal tech IPO. It would be a capital markets event closer to a sovereign-scale financing. The reason is simple: frontier AI companies need extreme capital for compute, data centres, chips, inference, safety, talent, and distribution. The risk is that public investors will ask for clearer proof of margins, not just revenue growth. An excellent collection of learning videos awaits you on our Youtube channel.

4. Anthropic has become the surprise valuation leader

Anthropic raised $65 billion in Series H funding at a $965 billion post-money valuation, surpassing OpenAI’s March valuation. Reuters also reported Anthropic’s annual revenue run-rate at more than $47 billion and said the company is preparing for a public market debut.

5. Anthropic’s ground situation is demand plus infrastructure pressure

Anthropic’s valuation is being driven by enterprise adoption of Claude, especially coding and professional-work use cases. But the ground situation is not only product demand. Reuters also reported that Apollo and Blackstone were working on about $36 billion in debt financing for Anthropic’s infrastructure expansion, including Google TPU purchases and leasing structures. That shows the core reality of frontier AI: growth requires huge balance-sheet engineering.

6. Cerebras is the clearest completed AI IPO case study

Cerebras priced its IPO at $185 per share, selling 30 million shares and raising $5.55 billion. Reuters reported a fully diluted valuation of $56.43 billion, making it the largest IPO of 2026 to that point. Cerebras shares began trading on Nasdaq under ticker CBRS on 14 May 2026, according to the company. A constantly updated Whatsapp channel awaits your participation.

7. Cerebras proves public investors will pay for AI infrastructure

Cerebras is not a consumer chatbot company. It is an AI chip and systems company competing in the Nvidia-centred infrastructure layer. Reuters reported that Cerebras revenue rose to $510 million in 2025 from $290.3 million in 2024. That means the IPO was not based on a mature profit profile. It was based on growth, AI infrastructure scarcity, and investor appetite for Nvidia alternatives.

8. Databricks is the most conventional “IPO-ready” AI company

Databricks is different from OpenAI and Anthropic. It has a clearer enterprise software profile, existing large customers, and a more familiar revenue model. In February 2026, Databricks said it completed a roughly $5 billion fundraise at a $134 billion valuation. Reuters reported that its annualized revenue run-rate rose 65 percent to $5.4 billion in Q4.

9. Databricks has stronger financial discipline signals

Databricks itself said it had surpassed a $5.4 billion revenue run-rate, was growing more than 65 percent year over year, had positive free cash flow over the last 12 months, had crossed a $1.4 billion revenue run-rate for AI products, and had net retention above 140 percent. These are the kinds of metrics public SaaS investors understand more easily than raw model-lab hype. Excellent individualised mentoring programmes available.

10. CoreWeave remains the public-market warning and benchmark

CoreWeave went public in March 2025, pricing at $40 per share, selling 37.5 million shares, and raising $1.5 billion. The company said the proceeds were for expanding its AI cloud platform. Yahoo Finance reported that this implied a roughly $23 billion fully diluted valuation and that the company had originally aimed for a larger raise.

CoreWeave matters because it showed both sides of the AI IPO trade: huge demand for GPU cloud exposure, but also public-market caution around debt, customer concentration, capex intensity, and margins.

11. SpaceX is AI-adjacent, not a pure AI IPO

SpaceX is often mentioned in the same 2026 mega-IPO conversation because of its scale and Elon Musk’s AI ecosystem, including xAI links. But it should not be treated as a pure AI listing. Reuters reported on 15 May 2026 that SpaceX was targeting a roughly $1.75 trillion IPO valuation, potentially the biggest-ever U.S. stock market debut.

12. Sierra shows the next layer: enterprise AI agents

Sierra is not in the same IPO class as OpenAI or Anthropic yet, but it matters because it represents enterprise AI agents. Sierra announced in September 2025 that it had raised $350 million at a $10 billion valuation. Economic Times reported in May 2026 that Sierra raised $950 million at a valuation above $15 billion.

This is the “application layer” of the AI IPO pipeline: customer service agents, enterprise automation, workflow bots, and industry-specific AI systems. Subscribe to our free AI newsletter now.

13. Scale AI is strategically important, but IPO visibility is weaker

Scale AI is still private and strategically important because it sits in the data, evaluation, and AI infrastructure layer. Reuters reported in 2025 that Meta acquired a 49 percent stake for $14.3 billion, valuing Scale AI at $29 billion, and that Alexandr Wang moved into a Meta superintelligence role while staying on Scale’s board.

For May 2026, Scale AI looks more like a strategic AI asset than a clean IPO candidate. Its Meta-linked ownership structure may complicate a straightforward public listing.

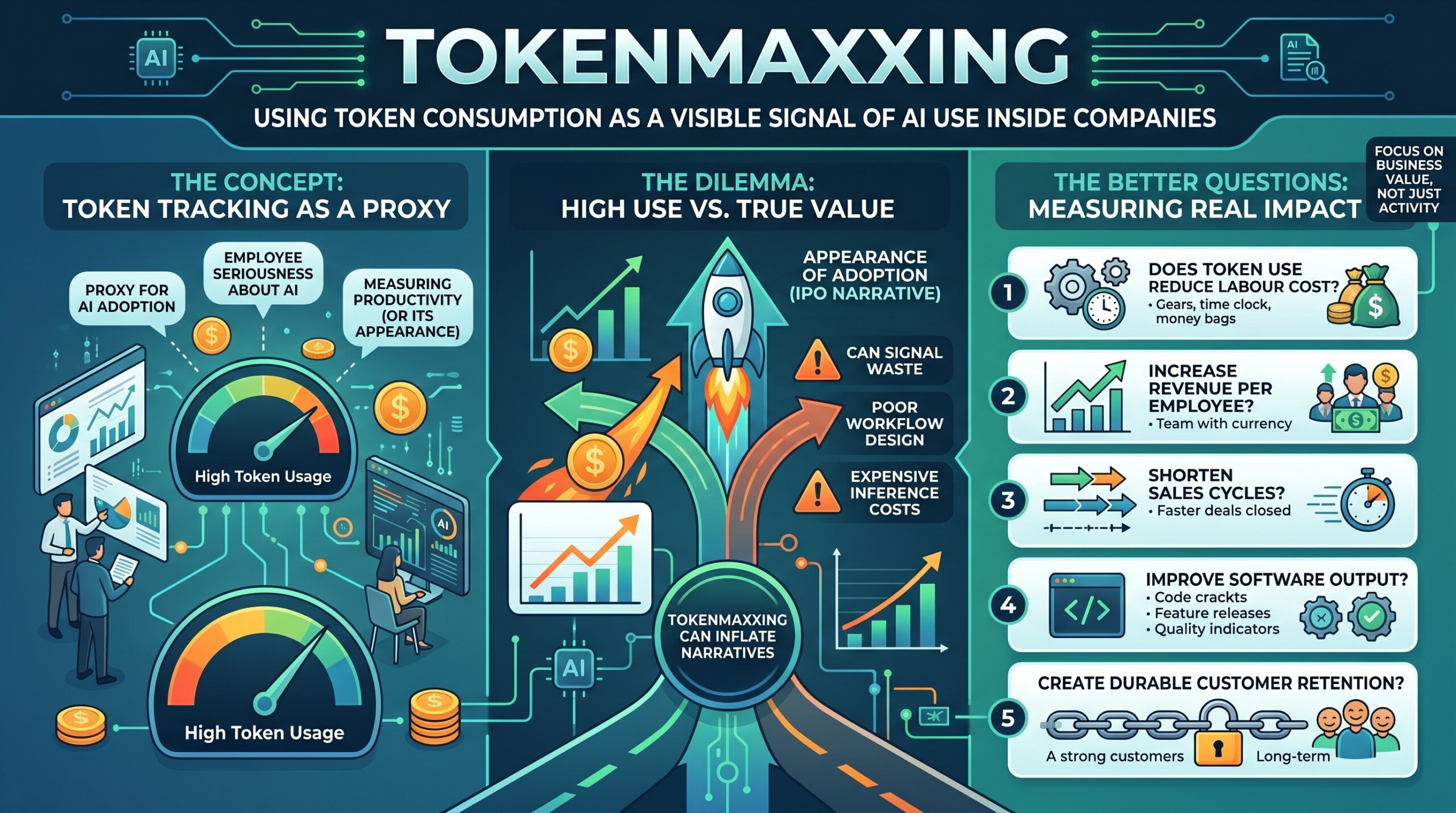

14. “Tokenmaxxing” is a real 2026 workplace signal, but also a bad valuation metric

Tokenmaxxing means maximizing or tracking AI-token usage as a proxy for AI adoption, productivity, or employee seriousness about AI. Recent commentary describes it as the practice of using token consumption as a visible signal of AI use inside companies.

For IPOs, tokenmaxxing can inflate narratives. High token use may show adoption, but it can also show waste, poor workflow design, or expensive inference. The better questions are: does token use reduce labour cost, increase revenue per employee, shorten sales cycles, improve software output, or create durable customer retention?

15. The real 2026 test is not hype, but unit economics

The mega AI IPO story is not just “big valuations”. It is a test of whether public markets will accept frontier AI economics. OpenAI and Anthropic may command near-trillion-dollar valuations, but they also face enormous compute costs. Cerebras has shown that public investors will fund AI infrastructure. Databricks shows that AI plus enterprise software can produce more familiar SaaS-style metrics. CoreWeave shows that public markets can be enthusiastic but still cautious. Upgrade your AI-readiness with our masterclass.

Conclusion

The factual May 2026 picture is this: AI IPOs are no longer theoretical, but the winners will need to prove revenue quality, gross margins, customer retention, compute efficiency, and defensible product advantage. The bubble question will not be answered by valuations. It will be answered by whether these companies can turn massive token consumption into durable cash flow.

Share this with the world

Related Articles

{kind=link}

{kind=link}

{kind=link}